Homeownership has always been the first rung on the ladder leading to household wealth. As Freddie Mac recently posted:

“Homeownership has cemented its role as part of the American Dream, providing families with a place that is their own and an avenue for building wealth over time. This ‘wealth’ is built, in large part, through the creation of equity…Building equity through your monthly principal payments and appreciation is a critical part of homeownership that can help you create financial stability.”

Home equity is the difference between the current market value of your house and the amount you currently owe on your mortgage. To estimate your equity, subtract your mortgage balance from the market value of your home.

You can find what you owe on your mortgage by looking at your last monthly statement or by contacting your lender. If you need help determining the current market value of your home, contact a local real estate professional.

Is homeownership truly a better path to wealth than renting?

Some argue that renting eliminates the cost of property taxes and home repairs. Every potential renter must realize that all the expenses the landlord incurs (property taxes, repairs, insurance, etc.) are already baked into the rent payment – along with a profit margin. You don’t save money by renting.

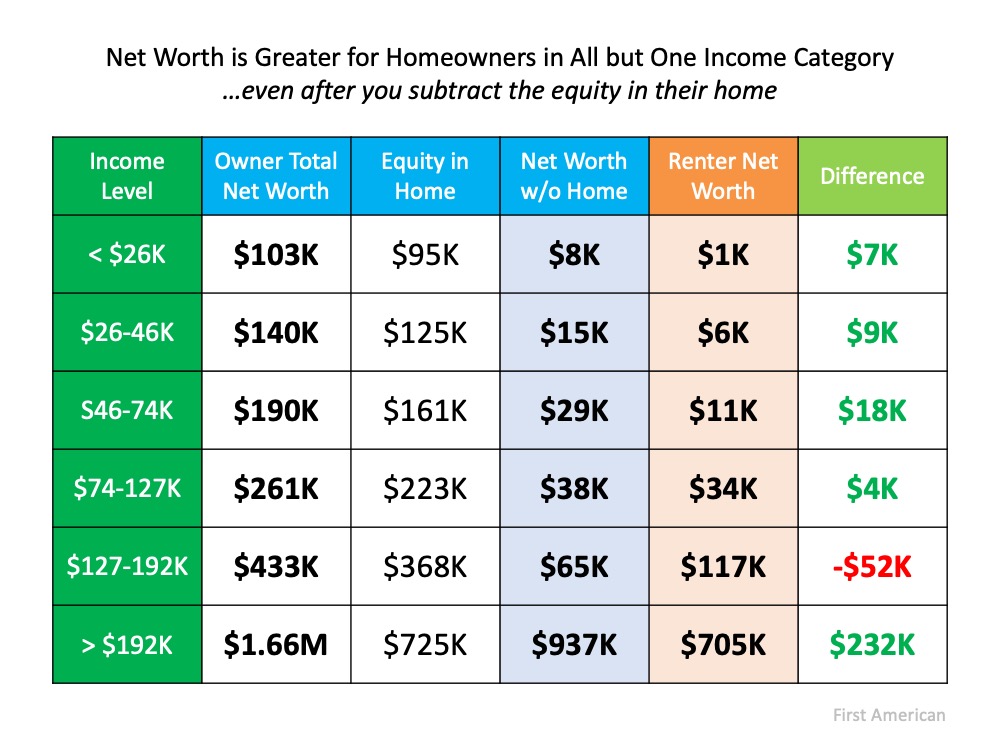

As proof of this, First American broke down the net worth of homeowners and renters by income categories. Here are their findings: Only one income category ($127-192K) has a higher net worth for renters over homeowners. Every other category shows that being a homeowner leads to greater accumulated wealth.

Only one income category ($127-192K) has a higher net worth for renters over homeowners. Every other category shows that being a homeowner leads to greater accumulated wealth.

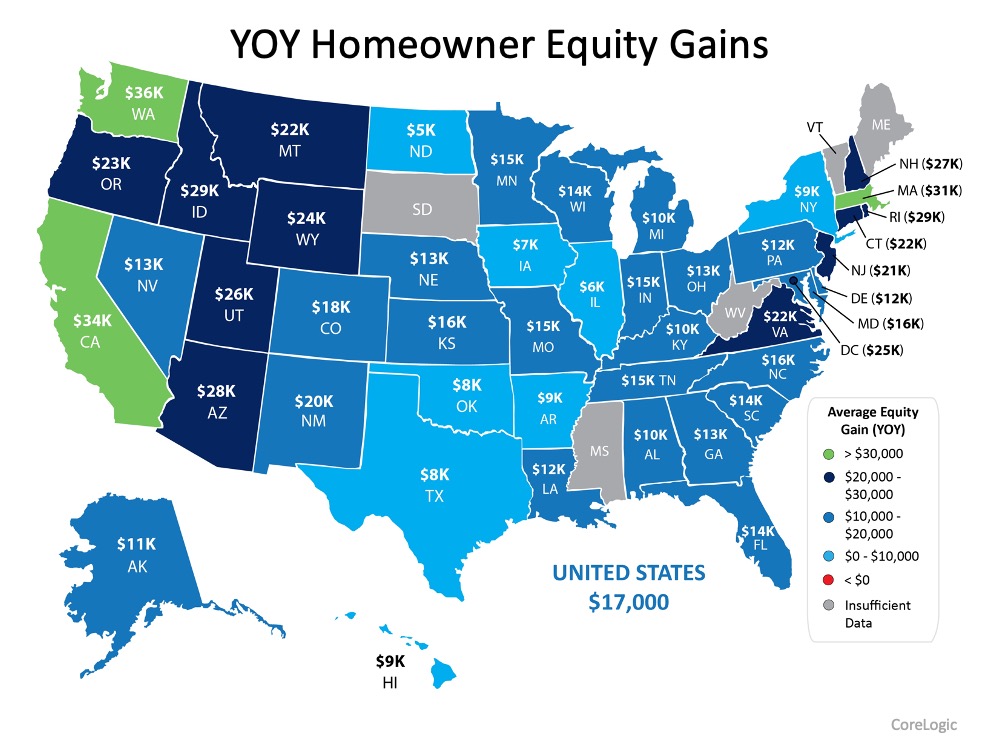

According to the latest Homeowner Equity Insights Report from CoreLogic, the average homeowner gained $17,000 in equity in just the last year. Here’s a breakdown of the year-over-year equity gain by state:

When can you cash in on your housing wealth?

Your home equity is part of your total wealth as a homeowner. The two most common ways homeowners can leverage their wealth are:

Selling: When you decide to sell your home, the equity you’ve built over time will come back to you in the sale. For example, if you paid off your $200,000 mortgage and sold your home for $350,000, you would receive $150,000 after closing.

Refinancing: You can refinance your current mortgage and take out some of the equity you have accumulated. With today’s historically low mortgage rates, you may be able to take out substantial cash and keep your monthly payment the same. Thankfully, homeowners today are doing this responsibly and not repeating the same mistakes made in 2006-2008 when some cashed out their entire equity to purchase luxury items like new cars, lavish vacations, etc.

How can these options help homeowners?

During these difficult times, many households are struggling with their housing expenses. Homeowners, because of their equity, have better alternatives. Odeta Kushi, Deputy Chief Economist at First American, recently explained that homeowners financially impacted by the pandemic will not necessarily be faced with foreclosure:

“The foreclosure process is based on two steps. First, the homeowner suffers an adverse economic shock…leading to the homeowner becoming delinquent on their mortgage. However, delinquency by itself is not enough to send a mortgage into foreclosure. With enough equity, a homeowner has the option of selling their home, or tapping into their equity through a refinance, to help weather the economic shock.”

What might the future bring?

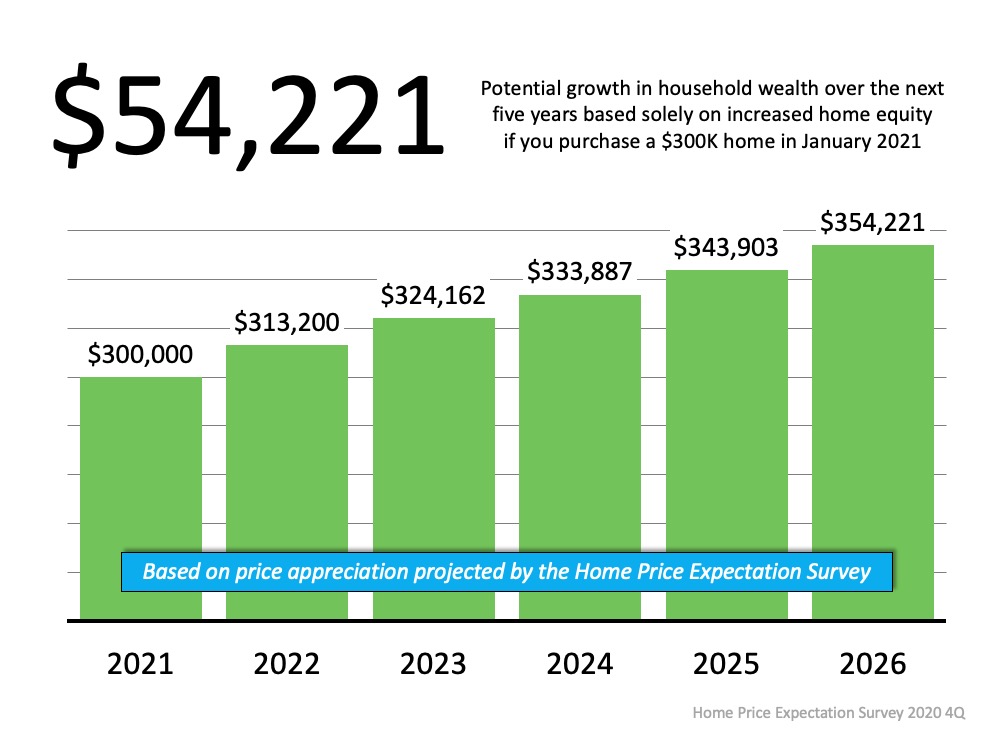

Most experts are calling for home prices to continue appreciating going forward. The Home Price Expectation Survey, a survey of a national panel of over one hundred economists, real estate experts, and investment & market strategists, indicates appreciation will continue for at least the next five years. Using their annual projections, the graph below shows the equity build-up a purchaser would potentially earn by buying a $300,000 home this January:

Bottom Line

Home equity, for most Americans, is the quickest way to build household wealth. That wealth gives homeowners more options during good times and in difficult situations.

There’s a lot of anxiety right now regarding the coronavirus pandemic. The health situation must be addressed quickly, and many are concerned about the impact on the economy as well.

Amidst all this anxiety, anyone with a megaphone – from the mainstream media to a lone blogger – has realized that bad news sells. Unfortunately, we will continue to see a rash of horrifying headlines over the next few months. Let’s make sure we aren’t paralyzed by a headline before we get the full story.

When it comes to the health issue, you should look to the Centers for Disease Control and Prevention (CDC) or the World Health Organization (WHO) for the most reliable information.

Finding reliable resources with information on the economic impact of the virus is more difficult. For this reason, it’s important to shed some light on the situation. There are already alarmist headlines starting to appear. Here are two such examples surfacing this week.

1. Goldman Sachs Forecasts the Largest Drop in GDP in Almost 100 Years

It sounds like Armageddon. Though the headline is true, it doesn’t reflect the full essence of the Goldman Sachs forecast. The projection is actually that we’ll have a tough first half of the year, but the economy will bounce back nicely in the second half; GDP will be up 12% in the third quarter and up another 10% in the fourth.

This aligns with research from John Burns Consulting involving pandemics, the economy, and home values. They concluded:

“Historical analysis showed us that pandemics are usually V-shaped (sharp recessions that recover quickly enough to provide little damage to home prices), and some very cutting-edge search engine analysis by our Information Management team showed the current slowdown is playing out similarly thus far.”

The economy will suffer for the next few months, but then it will recover. That’s certainly not Armageddon.

2. Fed President Predicts 30% Unemployment!

That statement was made by James Bullard, President of the Federal Reserve Bank of St. Louis. What Bullard actually said was it “could” reach 30%. But let’s look at what else he said in the same Bloomberg News interview:

“This is a planned, organized partial shutdown of the U.S. economy in the second quarter,” Bullard said. “The overall goal is to keep everyone, households and businesses, whole” with government support.

According to Bloomberg, he also went on to say:

“I would see the third quarter as a transitional quarter” with the fourth quarter and first quarter next year as “quite robust” as Americans make up for lost spending. “Those quarters might be boom quarters,” he said.

Again, Bullard agrees we will have a tough first half and rebound quickly.

Bottom Line

There’s a lot of misinformation out there. If you want the best advice on what’s happening in the current housing market, let’s talk today.

Many sellers believe spring is the best time to put their homes on the market because buyer demand traditionally increases at that time of year. What they don’t realize is if every homeowner believes the same thing, then that’s when they’ll have the most competition.

So, what’s the #1 reason to list your house in the winter? Less competition.

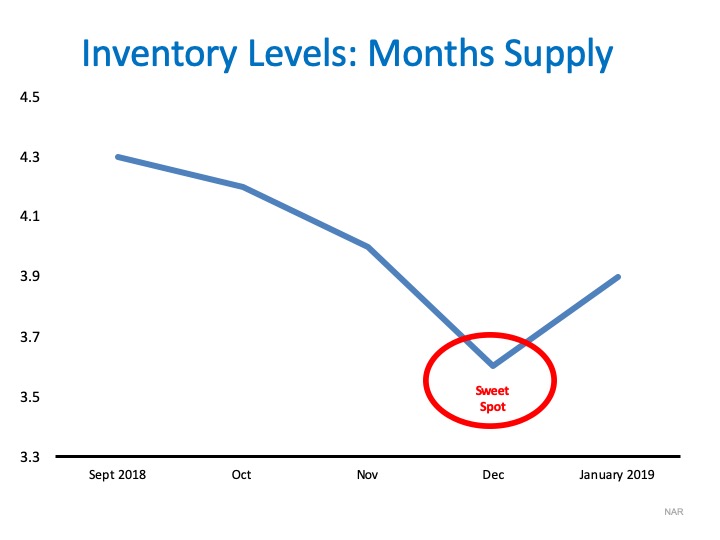

Housing supply traditionally shrinks at this time of year, so the choices buyers have will be limited. The chart below was created using the months supply of listings from the National Association of Realtors. As you can see, the ‘sweet spot’ to list your house for the most exposure naturally occurs in the late fall and winter months (November – January).

As you can see, the ‘sweet spot’ to list your house for the most exposure naturally occurs in the late fall and winter months (November – January).

Temperatures aren’t the only thing that heats up in the spring – so do listings! In 2018, listings increased from December to May. Don’t wait for these listings and the competition that comes with them to come to the market before you decide to list your house.

In 2018, listings increased from December to May. Don’t wait for these listings and the competition that comes with them to come to the market before you decide to list your house.

Added Bonus: Serious Buyers Are Out in the Winter

At this time of year, purchasers who are serious about buying a home will be in the marketplace. You and your family will not be bothered and inconvenienced by mere ‘lookers.’ The lookers are at the mall or online doing their holiday shopping.

Bottom Line

If you’ve been debating whether or not to sell your house and are curious about market conditions in your area, let’s get together to determine the best time to list your house.

Tom Petty famously penned the words, “the waiting is the hardest part” in his early 80’s hit song The Waiting, and his thought process can surprisingly also be applied to individuals considering selling their homes today. Traditional thinking would suggest it may be best to wait until the spring to sell when there is a flood of buyers in the market, but right now may in fact be an even better time to list your home.

We can see the overall economy is good: wages are rising, there are near record-low unemployment rates, and mortgage interest rates are still very low too. Over the past 10+ years the housing market has stabilized, so what (if anything) is the biggest challenge in the housing market today?

The answer is simple: it’s inventory.

According to the Existing Home Sales Report by the National Association of Realtors,

“Total housing inventory at the end of September sat at 1.83 million, approximately equal to the amount of existing-homes available for sale in August, but a 2.7% decrease from 1.88 million one year ago. Unsold inventory is at a 4.1-month supply at the current sales pace, up from 4.0 months in August and down from the 4.4-month figure recorded in September 2018.”

What does this mean?

While homes are coming to the market, they aren’t coming fast enough! Right now, across the country there is less than 6 months of overall inventory of homes for sale, putting us in a seller’s market. The challenge is that there are not enough homes for sale to increase the supply needed for the number of people who want to buy, especially in the starter and middle-level markets.

To be in a balanced market (meaning we have enough inventory for the number of buyers in the market), we need to have 6 months of inventory available. Today we are nowhere near that number, and as a matter of fact, the last time we reached that height was August 2012 (as shown in the graph below): When we look at the inventory challenge today, we can see that now is a great time to sell your house. Truthfully, waiting may end up being the hardest part in the long run. This landscape is a great place for sellers who own homes in the starter and middle-level markets to take the opportunity to sell in a sellers’ market, before inventory catches up with demand. Serious buyers are actively in the market and ready to make a move at this time of year. When inventory is limited at the lower end, like it is today, selling before more homes are listed could mean a significant seller’s advantage to those who are ready to move up. The upper level of the market has much more inventory available to move into, so it’s a win across the board.

When we look at the inventory challenge today, we can see that now is a great time to sell your house. Truthfully, waiting may end up being the hardest part in the long run. This landscape is a great place for sellers who own homes in the starter and middle-level markets to take the opportunity to sell in a sellers’ market, before inventory catches up with demand. Serious buyers are actively in the market and ready to make a move at this time of year. When inventory is limited at the lower end, like it is today, selling before more homes are listed could mean a significant seller’s advantage to those who are ready to move up. The upper level of the market has much more inventory available to move into, so it’s a win across the board.

Bottom Line

If you’re considering selling your home, don’t wait – now is the time to make your move! Take advantage of the high housing demand and the low inventory of homes for sale at the lower end of the market and use your purchasing power while mortgage rates are low to go after the move-up home of your dreams. Let’s get together to decide if now is the right time for you.

A considerable number of potential buyers shy away from the real estate market because they’re uncertain about the buying process – particularly when it comes to qualifying for a mortgage.

For many, the mortgage process can be scary, but it doesn’t have to be!

In order to qualify in today’s market, you’ll need a down payment (the average down payment on all loans last year was 5%, with many buyers putting down 3% or less), a stable income, and a good credit history.

Once you’re ready to apply, here are 5 easy steps Freddie Mac suggests to follow:

- Find out your current credit history and credit score– Even if you don’t have perfect credit, you may already qualify for a loan. The average FICO Score® for all closed loans in September was 737, according to Ellie Mae.

- Start gathering all of your documentation– This includes income verification (such as W-2 forms or tax returns), credit history, and assets (such as bank statements to verify your savings).

- Contact a professional– Your real estate agent will be able to recommend a loan officer who can help you develop a spending plan, as well as help you determine how much home you can afford.

- Consult with your lender– He or she will review your income, expenses, and financial goals in order to determine the type and amount of mortgage you qualify for.

- Talk to your lender about pre-approval– A pre-approval letter provides an estimate of what you might be able to borrow (provided your financial status doesn’t change) and demonstrates to home sellers that you’re serious about buying.

Bottom Line

Do your research, reach out to professionals, stick to your budget, and be sure you’re ready to take on the financial responsibilities of becoming a homeowner.